Ultimate Guide to Calculate FERS Retirement Benefits

Takeaways

Careful calculation of FERS retirement benefits ensures a financially secure retirement.

Understanding the components of FERS, such as the high-3 average salary and creditable service, is crucial for accurate benefit calculation.

Understanding FERS Retirement Benefits

The Federal Employees Retirement System (FERS) became effective January 1, 1987, for new federal civilian employees and was established in 1986. Associated with FERS is a Basic Benefit Plan, which guarantees pension payments to be derived on the basis of an employee’s salary and duration of service. Said contributions prepaidly finance the appropriate retirement allowances, thus forming part and parcel of the federal employee retirement system. Employee Contributions have varied throughout the years, ranging from 0.8% in 1987 to 4.4% more recently. The annuity pays out monthly annuity payments from the Basic Benefit Plan starting the first day of the month after retirement for the life of the retiree, with no duration certain feature. This is a major source of income which brings payment for life of the retired federal employee’s service. Perhaps most important amongst matters relating to FERS is the Thrift Savings Plan (TSP). The TSP is a defined contribution plan that supplements the Basic Benefit Plan with any tax-advantaged annuity and agencies shall contribute automatically 1% of basic pay. All these shall go towards having a super-strong retirement plan specifically catering for employees in their retirement age.

Calculating Your FERS Annuity

Figuring your FERS annuity is a rather complex process and requires at least some general knowledge of a few important things. This is because, in most cases, the main part of the FERS pension is calculated according to a commonly used formula in which the length of service plays an essential role. The number of years of service and the ‘high-3’ average salary determine most of your pension. Understanding these pieces of information could help a person come up with a rough estimate concerning their available retirement benefits. The method involves determining your high-3 average salary, working out your total creditable service, identifying points that lead to variations in your pay, and then using the appropriate retirement fraction. Each of these factors plays a fundamental role in determining the total sum that would be paid to you under the FERS annuity and making sure you get the right remuneration in your retirement years.

Calculating High-3 Average Salary

The high-3 average salary is multiplied by .01 and then by the first $22,000 of your total service and then by .011, from year 22,001 through 44,000, then .012 for 44,001 to 66,000 and soon at different intervals. This figure is derived by dividing the total basic pay received at the highest rate of pay by the number of years of creditable service; it doesn’t take into account changes in salary rates over time. The high three also does not count bonuses or overtime earned during those years to be part of the high three consecutive years. These estimates can give a rough forecast on future benefits to employees who would otherwise work without any clue on what lies ahead. Good calculation of the high-3 average salary therefore enhances your FERS annuity benefits.

Understanding Creditable Service

Creditable service may generally be defined as combinations of federal service creditable toward FERS retirement. Normally, this includes FERS deductions, pre-1989 service with redeposits, and all sick leave at their credit. Years of creditable service shall be rounded down to the nearest whole month based upon years, months, and days actually worked as an employee rounded this includes creditable civilian service. A deposit of 1.3% of your salary is required to include pre-1989 service in your FERS credit. Employees retiring after December 31, 2013, can use 100% of their unused sick leave for additional service credit. It should be pointed out, though, that while unused sick leave is counted as creditable service, it does not impact the high-3 average salary. Add together your month, day, and retirement year, subtract the latter from the current year to get your years, months, and days of service. Subtract your last RSCD date from your current RSCD, then add the result to all bought military time and sick leave to the total RSCD for full computation of total service time.

Factors Affecting Average Pay and the Retirement Factor

Various factors can affect the computation of your average pay, which is so important in ascertaining your FERS annuity. Average pay, for the purposes of FERS computation, involves basic pay, plus locality pay, and shift rates. Depending on your location, locality pay, combined with basic pay, helps determine your average pay. 'High-3' Average Pay This is done by averaging the highest basic pay. It does this over any three consecutive years of service. Averaging the highest 36 months of basic pay would reflect more accurately the salary received during the years of greatest income. Multiplying by the ‘Retirement Factor’ The retirement factor is a vital piece in calculating your FERS annuity and determining your overall benefit. Typically, federal employees use a retirement factor of 1% or 1.1%. The total high-3 average pay multiplied by years of service and, for someone retiring at age 62 or later with at least 20 years of service, then it's 1.1% of the high-3 average pay multiplied by years of service. For workers under age 62, the calculation formula for the FERS pension is 1.1% times high-3 average salary years of creditable service. If you retire before 60 with less than twenty years of service, there will be a reduction of 5% for each year under age 62. Those retiring at age 62 with 20 or more years of service receive an additional 10% in their pension calculation. Knowing how the retirement factor applies helps you plan your retirement date to maximize benefits.

Minimum Retirement Age (MRA) for FERS

The regulation as to the Minimum Retirement Age under FERS for all federal employees is a very crucial one. For one to have that full and immediate retirement under FERS, there are attained ages and service prerequisites. The MRA varies by birth year whether 55 or 57 years old. However, the MRA at 10 years of service but less than 30 years will cause a 5 percent reduction in the benefit for each year less than age 62. If the employee has completed at least three years of service, that person will have attained an immediate MRA benefit once he attains age 62. You should, therefore, understand your MRA for you to understand how it affects your benefits during your retirement period.

Deferred and Postponed Retirement

Deferred and postponed retirement is another feature that is available in the federal employees’ retirement program, facilitating flexibility in an employee’s retirement plan. The former is applicable when a separation from the service is made before the MRA, while the latter applies where separation occurs after reaching the MRA. Each choice has different pros and cons. Opting for a postponed retirement helps avoid the penalty reduction of 5%. This can, in the end, boost your annual pension. It also keeps benefits like FEHB and FEGLI, which are untouched under deferred retirement. However, deferring retirement costs the interim COLA that would be forgone until annuity payments begin. Thus, these alternatives are instrumentally strategic for making choices appropriate to your retirement plans.

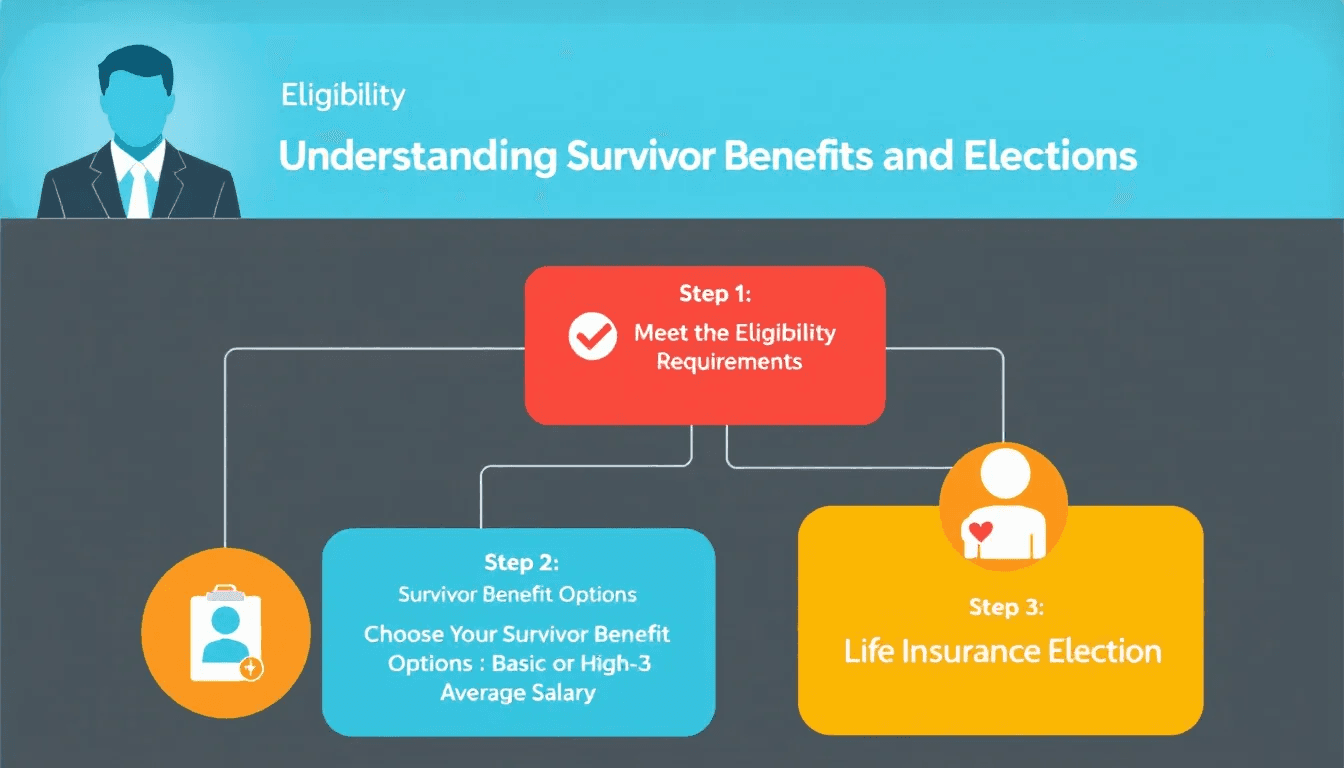

Survivor Benefits and Elections

Survivor benefits are one of the most important things when an individual is planning to retire from federal service. The selection of the survivor annuity election will determine most of the benefits that the spouse will get once the retired partner is dead, and hence it affects the monthly payments to be made to the retiree. For a maximum survivor annuity, there is a 10% reduction in the monthly payment of the retiree and gives 50% of the unreduced annuity to the survivor upon retirement. Selection of a partial survivor annuity shall reduce the participant’s monthly payment by 5%; thus, the spouse shall get 25% of the unreduced annuity in case the participant dies. If an employee is married when he or she retires from federal service, then spousal consent must be given to any election in which anything less than full survivor annuity is provided. These are some of the options that will assure your beloved ones’ financial safety after your death.

Disability Retirement under FERS

While the retirement under the disability provision is unfavorable, the federal employee, in case he comes to be disqualified to continue working because of a severe case of handicap, is ensured of the basic financial protection. This calculation will yield 60 percent of one’s average “high-3” salary for the first year in retirement, less any social security benefits that would accrue to the individual during that month and year. After the first year, this reverts to 40 percent; then not of the average high-3 years’ salary but 60 percent of social security disability benefits. There shall be a re-computation, however, after 12 months and at age 62. While total service used in the computation if for a regular FERS annuity includes time as a FERS disability annuitant, which augments the years of creditable service. An employee will continue to receive a portion of their salary cost until such period when they will be supposed to receive regular retirement pension in full upon reaching 62 years old.

Cost of Living Adjustments (COLA) and Special Retirement Supplement

Excepted benefits: Cost of Living Adjustments (COLA) are meant to help retirees keep their purchasing power as the price level inflates. Generally, FERS retirees under 62 do not qualify for COLA, unless a particular set of criteria is met. Those with less than one year in receipt of benefits shall receive a COLA prorata Knowing how COLAs work helps retirees make financial plans for the future and prepare for changes in benefits. These adjustments will help ensure that retirees will be able to live comfortably even as the costs of living increase. It may be said to bridge individuals to social security at the age of 62. Retirees under FERS may receive this supplement if they retire before 62 and are eligible for an immediate unreduced retirement. At retirement, approximately one-half of FERS annuitants qualify for the Special Retirement Supplement. It is paid equal to that Social Security benefit earned from Federal service and stops on their 62nd birthday. There is no application for this Supplement but a post-retirement income test on the FERS Special Retirement Supplement can reduce benefits. The Special Retirement Supplement therefore is part of the regular FERS retirement system, requiring no application for it to be paid.

Impact of Military Service on FERS Retirement

Military service can have an impact on FERS retirement benefits if properly credited. Specifically, military service is creditable to FERS provided it was honorable and was performed on an active basis. Thus, under USERRA, any person returning from military service shall return to his former position and may also receive credit for his service under FERS. Military service performed after 1956, to be credited by FERS, requires a deposit based on his military basic pay. These deposits for military service are to be paid before the termination of government employment, as a qualification for receiving credit towards retirement. Awareness of these requirements will help in the accurate accounting of military service in your FERS benefits.

Retirement Calculators and Benefit Estimates

The Average American Can Retire at Age 63 – How Do You Compare? A retirement calculator is an essential online planning tool for any federal employee intending to retire. Any input from the user will lead to the provision of possible scenarios on retirement based on the given data. This can show how changes in salary or years of service will impact the retirement pay. It is supposed to use it with their service history as well as salary information to get accurate calculations. The FERS retirement calculation calculator is very strict and efficient in its operations of calculating benefits; thus, it is a must-have during your retirement planning.Obtaining a FERS Benefit Estimate Requesting a FERS benefit estimate is integral to retirement planning. You should fill out the appropriate documentation available from OPM to receive an estimate. The forms will require very detailed information concerning your history of employment as well as any documentation related to service. OPM, in providing the benefit estimate, could help identify claimed service differences that could affect your retirement benefits. Obtaining an estimate, be sure to check licensed financial planners to put together a comprehensive retirement strategy.

Early Retirement Options

Early Retirement Options. The early retirement options extend flexibility to federal employees who wish to opt for an early exit from federal service. The Voluntary Early Retirement Authority is a temporary provision used to lower age and service requirements for retirement during a major reorganization of federal agencies. Any employee who has completed at least 20 years of service and reached the age of 50 can retire under VERA. Retirement is also allowed for employees who have clocked in 25 years of service irrespective of age. The VERA provision does not reduce the annuity of a FERS employee otherwise eligible for immediate retirement. It is a way to get out of the service early without substantial financial penalties. And, thus, more control over the retirement plan. An optimal retirement date can help in maximizing pension benefits under FERS. To maximize pension benefits under FERS, you basically should retire on December 31, and get a fresh start in the New Year, which aligns well with financial planning. An informed decision as to when to retire will maximize benefits as well as ensure a smooth transition; the following shall also apply Standard Treatment for Law Enforcement Officers and Other Special Categories of Employees

Special Categories of Employees

FERS Law Enforcement Officers are treated as being under special provisions and thereby become eligible for improved retirement benefits. Normally, this includes making some allowances to their retirement ages and due to the nature of their work, they have different methods of calculation than regular federal workers. Similarly, with Air Traffic Controllers or any other position requiring specialized skills, it falls under special categories with different calculations for retirement. Such unique considerations provide the basis upon which such employees can effectively plan their retirement. A comprehensive financial plan is very important to federal employees as this will help them prepare to transition into retirement securities. Early financial planning can help federal employees maximize their retirement benefits without having any last-minute decisions involving the federal government. Employees can capitalize upon resources from their agency that can further enhance the preparation for their retirement, such as retirement workshops and financial advising services. They can also utilize retirement calculators to estimate retirement income and assess financial readiness. Workers should weigh their exit time, for which it will be necessary to understand the tax implication and benefits.

Summary

In conclusion, knowledge and calculation of your retirement benefits make all the difference between a financially sound retirement and one fraught with the uncertainties of potential economic insecurity in old age. Every detail of FERS-from high-3 average salary determination to wise calculation of the effect of military service on employees playing their roles most constructively towards prudent retirement planning. Make the best use of the FERS retirement calculator and financial advisors to get to your maximum benefits. Remember, early planning and well-informed decisions are what make a successful and fulfilling retirement.

Frequently Asked Questions

What formula does OPM use to find the high-3 average salary?

The high-3 is obtained by averaging the highest rates of basic pay received over any three consecutive years of service to the Federal Government. This would ensure the formula is sensitive enough to pick out the period when basic pay rates were the maximum for that employee.

Who meets the eligibility criteria for the Special Retirement Supplement?

An individual must meet the following conditions for a Special Retirement Supplement under FERS: having retired before the age of 62 with an immediate and unreduced retirement benefit. Creditable military service is active and honorable toward FERS retirement, provided that deposits based on military basic pay are made before separating from federal employment for most of his or her career.

Why is Choosing the Right Retirement Date Important?

Selecting the right date of retirement is extremely important for getting full pension benefits and a smooth financial transition into retirement. This decides the overall financial security and quality of post-retirement life.